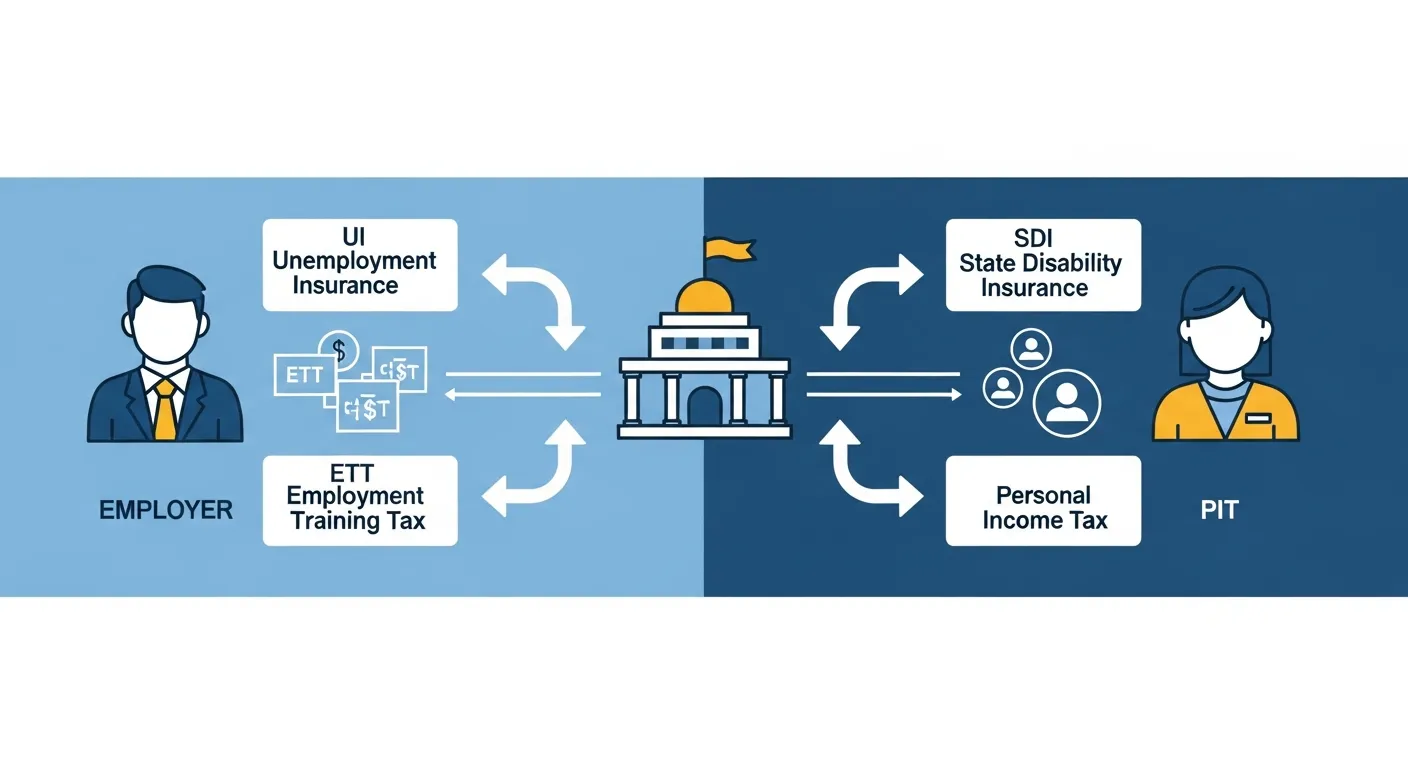

California employers face one of the most complex payroll tax systems in the country. Between state disability insurance, unemployment insurance, employment training tax, and personal income tax withholding, there are four separate state-level taxes to track, each with its own rate, wage base, and filing requirements.

Need help with California payroll taxes? Contact Clear Peak Accounting today.

If you run payroll in California, or plan to hire your first employee here, this article breaks down every payroll tax you need to know about for 2026: what each tax is, who pays it, the current rates, how to file, and the penalties you face for getting it wrong.

Key takeaway: California has four state payroll taxes administered by the Employment Development Department (EDD). Two are paid by the employer (UI and ETT), and two are withheld from employee wages (SDI and PIT). All four are reported quarterly through EDD e-Services for Business.

The Four California Payroll Taxes at a Glance

Every California employer is responsible for four state payroll taxes. The table below summarizes the 2026 rates and wage limits:

| Tax | Who Pays | 2026 Rate | Taxable Wage Limit | Max Annual Cost Per Employee |

|---|---|---|---|---|

| UI (Unemployment Insurance) | Employer | 1.5% to 6.2% (new employers: 3.4%) | First $7,000 | $434 (at highest rate) |

| ETT (Employment Training Tax) | Employer | 0.1% | First $7,000 | $7 |

| SDI (State Disability Insurance) | Employee (employer withholds) | 1.3% | No cap, all wages | No maximum |

| PIT (Personal Income Tax) | Employee (employer withholds) | 1% to 13.3% (varies) | No cap | No maximum |

The first two taxes (UI and ETT) are direct employer expenses. The last two (SDI and PIT) are employee obligations, but you are responsible for withholding them from each paycheck and remitting them to the state.

Let’s look at each one in detail.

State Unemployment Insurance (UI)

Unemployment Insurance is the largest employer-paid payroll tax in California. It funds temporary benefits for workers who lose their jobs through no fault of their own.

How UI works:

- Employers pay UI on the first $7,000 of wages per employee per calendar year

- New employers are assigned a flat rate of 3.4% for their first two to three years

- After that, your rate is based on your “experience rating,” which reflects your claims history

- Experienced employer rates range from 1.5% to 6.2% under the 2026 Schedule F+

- EDD mails your assigned rate on Form DE 2088 each December

What this costs in practice:

For a new employer with 10 employees, UI costs roughly $238 per employee per year, or $2,380 total. At the maximum rate of 6.2%, that rises to $434 per employee, or $4,340 for a 10-person team.

Once an employee’s year-to-date wages exceed $7,000, you stop paying UI on their additional earnings for that calendar year.

Employment Training Tax (ETT)

The Employment Training Tax is a small, flat-rate employer tax that funds workforce training programs across the state.

- Rate: 0.1% (one-tenth of one percent)

- Wage base: First $7,000 per employee per year (same as UI)

- Maximum cost: $7 per employee per year

- Who pays: Employer only

ETT is reported alongside UI on your quarterly filings. At $7 per employee annually, it is a minimal expense, but it is still a required tax. Every employer subject to UI also pays ETT.

State Disability Insurance (SDI)

State Disability Insurance provides temporary wage-replacement benefits to employees who cannot work due to non-work-related illness, injury, or pregnancy. SDI also funds California’s Paid Family Leave (PFL) program.

Key SDI facts for 2026:

- Rate: 1.3% (increased from 1.2% in 2025)

- Wage cap: None. All wages are subject to SDI since January 1, 2024

- Who pays: This is an employee tax. Employers withhold it from each paycheck and remit it to EDD

- DI/PFL max weekly benefit: $1,765 for 2026

The elimination of the SDI wage cap in 2024 was a significant change. Previously, SDI only applied to a portion of wages. Now, a high-earning employee will have SDI withheld on their entire salary with no ceiling.

Example: An employee earning $150,000 per year will have $1,950 in SDI withheld annually (150,000 x 1.3%). There is no point during the year where the withholding stops.

Personal Income Tax (PIT) Withholding

California Personal Income Tax withholding works similarly to federal income tax withholding, but uses the state’s own progressive tax brackets and withholding schedules.

- Rates: Range from 1% to 13.3%, depending on the employee’s income and filing status

- Wage cap: None. PIT applies to all wages

- Who pays: Employee (employer withholds and remits)

- Withholding basis: Employee’s DE 4 form (California’s version of the federal W-4)

Employers determine the correct PIT withholding amount using EDD’s published withholding schedules. For 2026, EDD provides two methods:

- Method A (Wage Bracket): Look up the withholding amount in a table based on wages and filing status

- Method B (Exact Calculation): A formula-based approach for greater precision

Important 2026 change: The PIT deposit threshold dropped from $500 to $400. If your accumulated PIT withholding reaches $400, you must deposit it on the next business day (for next-day depositors) or follow the semi-weekly schedule. Missing this threshold change is a common penalty trigger.

Employer vs. Employee Responsibilities

Understanding who pays what is critical to running payroll correctly in California:

Let Clear Peak Accounting handle your California payroll tax compliance. Contact us today.

Employer pays directly:

– UI: 1.5% to 6.2% on first $7,000

– ETT: 0.1% on first $7,000

– Combined maximum: $441 per employee per year

Employer withholds from employee wages and remits to EDD:

– SDI: 1.3% on all wages (no cap)

– PIT: Variable rate on all wages (no cap)

The employer’s total obligation goes beyond just “paying” taxes. You are also responsible for:

– Calculating correct withholding amounts each pay period

– Depositing withheld taxes on time based on your deposit schedule

– Filing quarterly returns (DE-9 and DE-9C)

– Reporting new hires to the California New Employee Registry within 20 days

– Maintaining accurate payroll records for at least four years

If you’re managing business accounting and management across multiple areas, staying on top of payroll tax obligations is one of the most time-sensitive responsibilities.

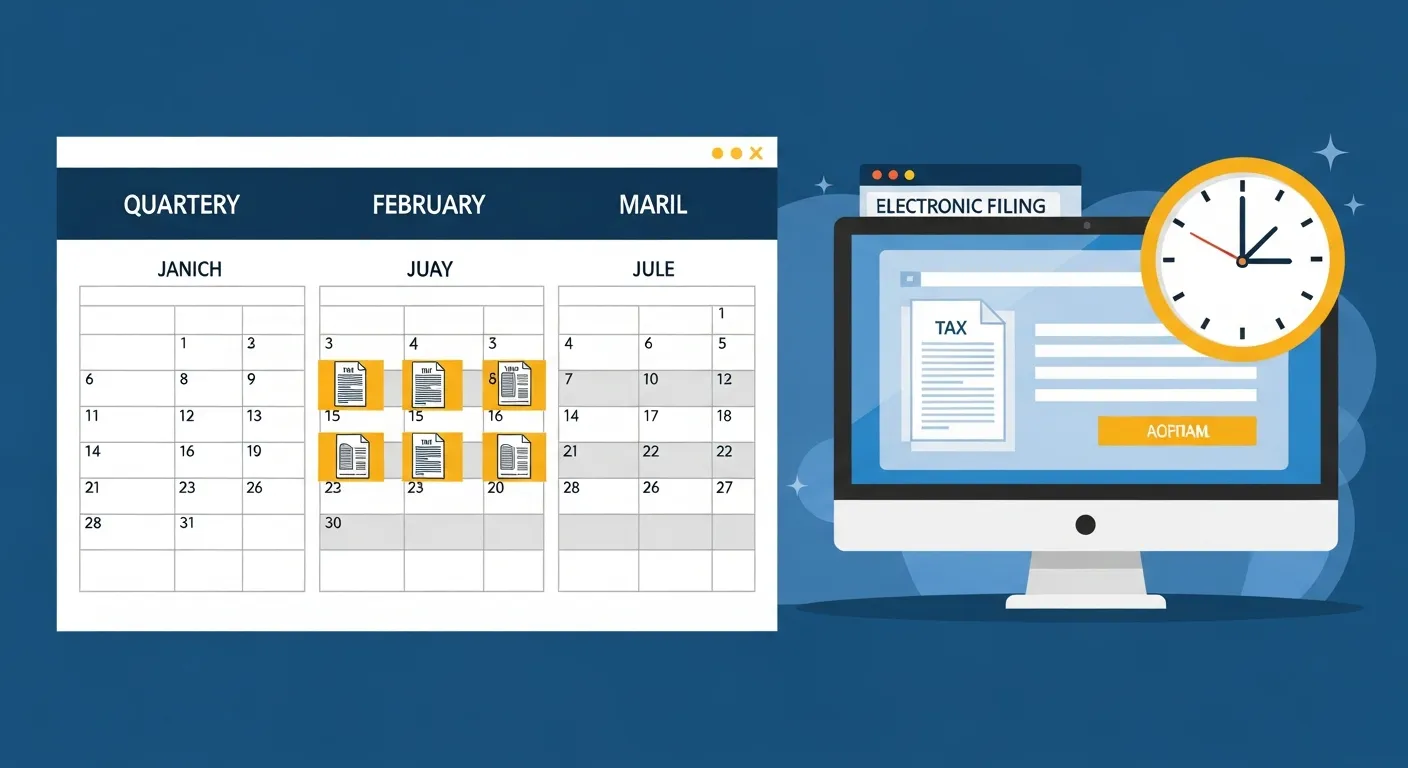

DE-9 and DE-9C Filing Requirements

California employers must file two quarterly reports with EDD:

DE-9 (Quarterly Contribution Return and Report of Wages):

– Reports total wages paid and taxes owed for the quarter

– Shows UI, ETT, SDI, and PIT amounts

– This is the form you use to reconcile your quarterly tax liability

DE-9C (Quarterly Contribution Return and Report of Wages, Continuation):

– Lists each employee by name and Social Security number

– Reports individual employee wages for the quarter

– Filed as a continuation/attachment to the DE-9

2026 Quarterly Filing Deadlines:

| Quarter | Period | Due Date |

|---|---|---|

| Q1 | January through March | April 30, 2026 |

| Q2 | April through June | July 31, 2026 |

| Q3 | July through September | November 2, 2026 |

| Q4 | October through December | February 1, 2027 |

All filings and payments must be submitted electronically through EDD e-Services for Business. Paper filings are no longer accepted for most employers.

Note that the Q3 deadline is November 2 (not October 31) because the standard due date falls on a weekend in 2026.

How to Set Up Your EDD Payroll Tax Account

If you are a new employer in California, you must register with EDD before your first payroll filing. Here is the process:

-

Determine if you are an employer. You must register if you pay more than $100 in wages in a calendar quarter, or if you employ one or more people for any part of a day in 20 different weeks in a calendar year.

-

Register online. Use the EDD e-Services for Business portal to create your employer account. You will need your Federal Employer Identification Number (FEIN), business legal name, and address.

-

Receive your EDD account number. EDD will assign you an eight-digit employer account number. Keep this number; you will use it on every filing.

-

Get your UI rate notice (DE 2088). New employers receive a 3.4% UI rate. Each December, EDD mails your rate for the following year.

-

Set up your deposit schedule. Your deposit frequency depends on the amount of PIT withheld. Most small employers deposit quarterly, but you may be required to deposit semi-weekly or next-day if your withholding exceeds certain thresholds.

For businesses just getting started with payroll, consider working with a CPA firm that handles payroll management for startups to avoid costly setup mistakes.

Penalties for Late Filing and Payment

EDD takes payroll tax compliance seriously. Here are the penalties you face for falling behind:

Late payment penalty:

– Up to 15% of the unpaid tax amount plus interest

– Interest accrues from the original due date until the tax is paid

Late filing penalty:

– $50 or 15% of the amount due (whichever is greater) for late DE-9 and DE-9C filings

– Additional penalties for failure to report wages for individual employees

Other penalties:

– Failure to withhold: If you do not properly withhold SDI or PIT, you become personally liable for the amounts you should have withheld

– Fraud or willful evasion: Criminal penalties including fines and imprisonment

– Misclassification: Classifying employees as independent contractors to avoid payroll taxes can result in back taxes, penalties, and interest going back up to three years

The easiest way to avoid penalties is to file electronically through EDD e-Services, set up automated deposits, and keep your payroll records current.

Common Payroll Tax Mistakes California Employers Make

Even experienced employers make these errors. Watch out for:

1. Not updating the SDI rate for 2026. The rate increased from 1.2% to 1.3%. If your payroll system is still using the old rate, you are under-withholding from every employee.

2. Leaving an old SDI wage cap in the system. California eliminated the SDI wage cap in 2024. If your software still stops withholding SDI after a certain threshold, your employees are being under-withheld and you are liable for the difference.

3. Missing the new $400 PIT deposit threshold. The threshold for next-day and semi-weekly PIT deposits dropped from $500 to $400 in 2026. If you hit $400 in accumulated PIT withholding, you need to deposit immediately.

4. Using the wrong UI rate. Your UI rate changes every year based on your experience rating. Always check your DE 2088 notice in December and update your payroll system before your first January payroll.

5. Filing DE-9C with errors. Incorrect Social Security numbers, misspelled names, or wrong wage amounts on the DE-9C cause processing delays and potential penalties. Double-check employee data before filing.

6. Failing to report new hires. California requires you to report every new hire to the New Employee Registry within 20 days of their start date. Many employers forget this step or report late.

7. Misclassifying workers. California’s ABC test (under AB 5) makes it difficult to classify workers as independent contractors. If EDD determines a worker should have been classified as an employee, you owe back payroll taxes plus penalties.

Frequently Asked Questions

Talk to a California CPA about your payroll tax obligations. Contact Clear Peak Accounting.

How much is payroll tax in California for employers?

The total employer-paid payroll tax in California ranges from $112 to $441 per employee per year, depending on your UI rate. This covers UI (1.5% to 6.2% on the first $7,000) and ETT (0.1% on the first $7,000). In addition, employers must withhold and remit SDI (1.3% on all wages) and PIT (variable rate on all wages) from employee paychecks.

What is the SDI rate for 2026?

The California SDI rate for 2026 is 1.3%, up from 1.2% in 2025. There is no wage cap, meaning SDI is withheld on every dollar of wages an employee earns.

When are California payroll taxes due?

Quarterly filings (DE-9 and DE-9C) are due by the last day of the month following the end of each quarter: April 30, July 31, October 31 (November 2 in 2026 due to the weekend), and January 31 (February 1, 2027). SDI and PIT deposits may be required more frequently depending on your withholding amounts.

Do I need to register with EDD if I only have one employee?

Yes. If you pay wages of $100 or more in a calendar quarter, you must register with EDD and begin paying payroll taxes. There is no minimum employee threshold for registration.

What happens if I pay California payroll taxes late?

Late payments trigger a penalty of up to 15% of the unpaid tax amount, plus interest calculated from the original due date. Repeated or willful failures to pay can result in additional penalties.

Take the Complexity Out of California Payroll

California payroll tax compliance requires attention to detail, up-to-date rate tables, and timely filings every quarter. For many small business owners, managing payroll in-house means tracking four different taxes, multiple deadlines, and constantly changing rates.

If payroll tax compliance is taking time away from running your business, Clear Peak Accounting can help. Our team handles outsourced payroll for small businesses across California, including EDD filings, tax deposits, and quarterly reconciliation.

Contact us to learn how we can simplify your payroll.