California tax brackets can feel confusing because the state uses a progressive income tax system, adds a 1% Mental Health Services Tax for very high earners, and taxes many types of income that people may expect to be treated differently. If you live in California, moved here recently, sold investments, earned equity compensation, or run a business in the state, understanding where your income falls in the brackets is the first step toward smarter tax planning.

Connect with Clear Peak Accounting to discuss a California tax strategy tailored to your income, business, investments, and filing status.

This article explains the 2025 California income tax brackets for single filers, married couples filing jointly, and heads of household. It also covers what income California taxes, how the state compares with other states, deductions and credits that may reduce your liability, estimated tax rules, and planning strategies for high-income taxpayers.

How California Tax Brackets Work

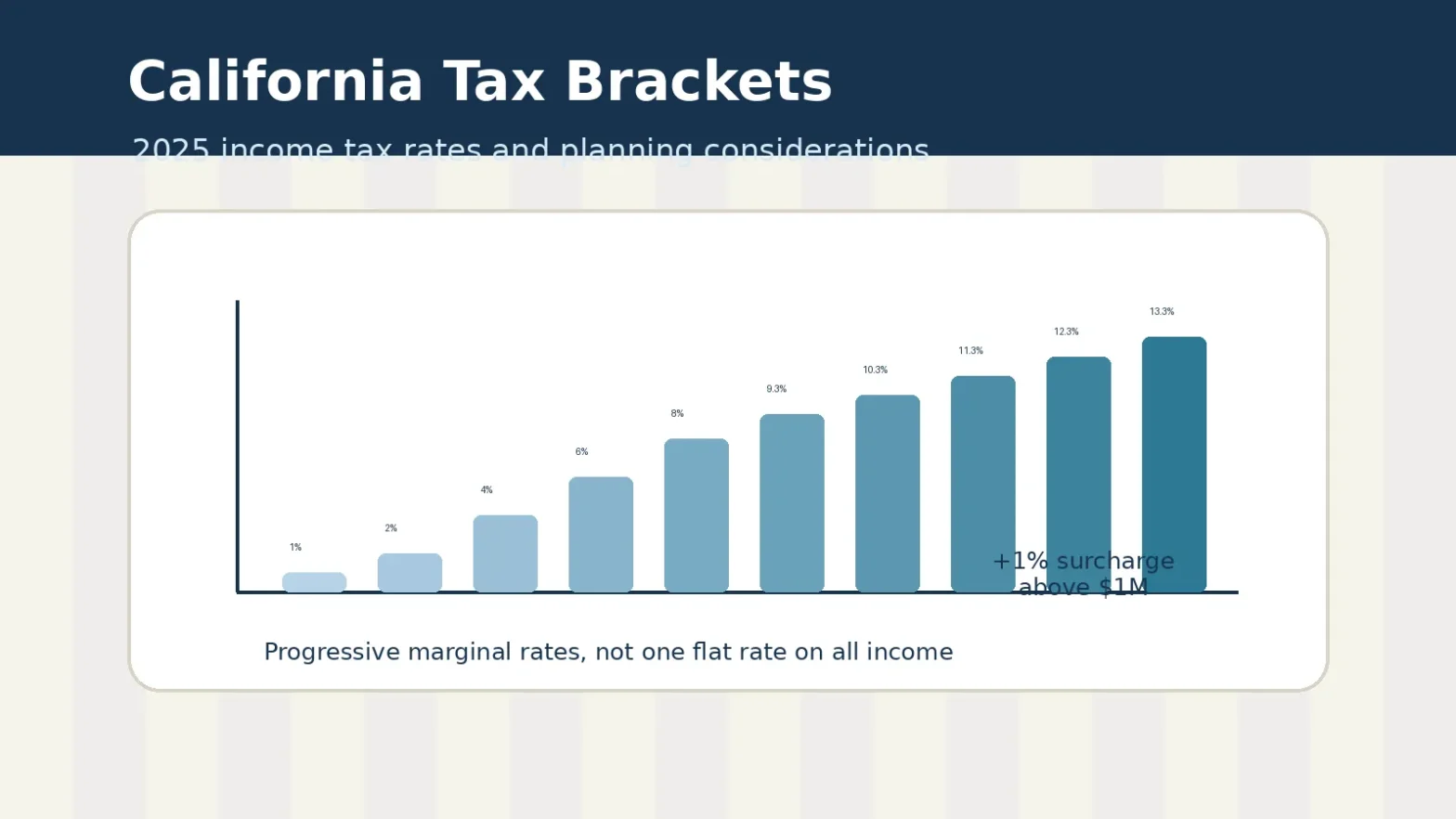

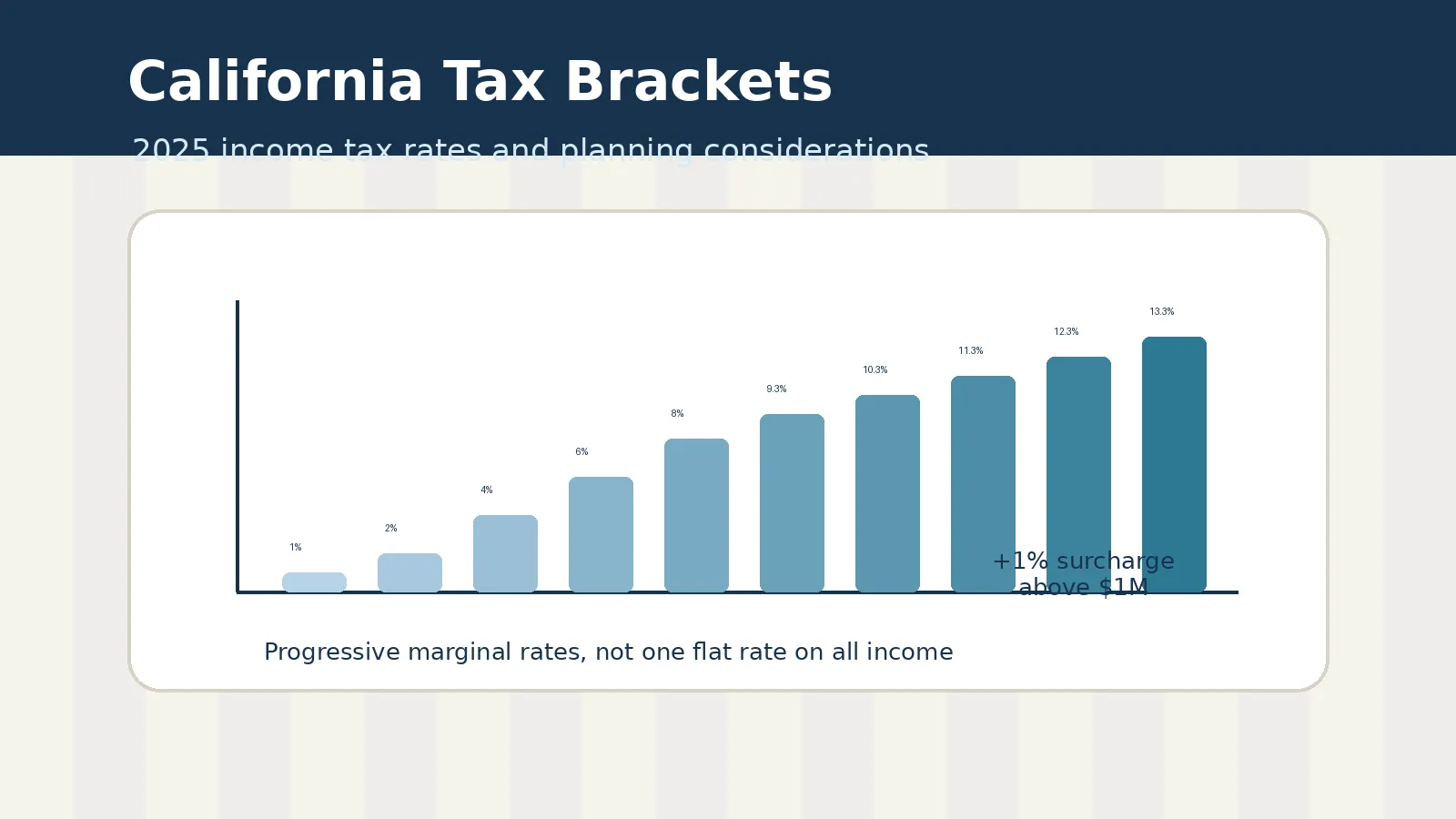

California tax brackets use a marginal rate system, which means each layer of taxable income is taxed at its own rate. You do not pay your highest rate on every dollar earned. Instead, income moves through the 1%, 2%, 4%, 6%, 8%, 9.3%, 10.3%, 11.3%, and 12.3% brackets as taxable income rises.

For example, a taxpayer whose income reaches the 9.3% bracket does not pay 9.3% on all taxable income. The first dollars are taxed at 1%, the next layer at 2%, then 4%, and so on. Only the dollars inside the 9.3% bracket are taxed at 9.3%.

That distinction matters for planning. A bonus, stock sale, Roth conversion, business profit increase, or capital gain may push only the additional income into a higher bracket. It does not retroactively increase the rate on all earlier income.

2025 California Tax Brackets for Single Filers

Single filers use their own California tax bracket schedule for 2025, and the brackets rise quickly once taxable income passes the middle-income ranges. The Franchise Tax Board publishes annual rate schedules, and single taxpayers should use taxable income, not gross income, when matching income to the correct marginal rate.

| Taxable Income | Marginal Rate |

|---|---|

| $0 to $11,079 | 1% |

| $11,079 to $26,264 | 2% |

| $26,264 to $41,452 | 4% |

| $41,452 to $57,542 | 6% |

| $57,542 to $72,724 | 8% |

| $72,724 to $371,479 | 9.3% |

| $371,479 to $445,771 | 10.3% |

| $445,771 to $742,953 | 11.3% |

| $742,953 to $1,000,000 | 12.3% |

| Over $1,000,000 | 13.3% effective top rate, including the 1% surcharge |

Single high-income professionals, founders, executives, investors, physicians, real estate professionals, and creators often reach the upper brackets through a combination of wages, business income, capital gains, equity compensation, and investment income. If your income changes significantly from year to year, proactive projections are important because withholding may not keep pace with the state liability.

2025 California Tax Brackets for Married Filing Jointly

Married couples filing jointly generally receive wider California tax brackets than single filers, but the top-rate planning issues remain significant. For 2025, joint filers should pay special attention to large income events, because the 1% Mental Health Services Tax can still apply once taxable income exceeds $1 million.

| Taxable Income | Marginal Rate |

|---|---|

| $0 to $22,158 | 1% |

| $22,158 to $52,528 | 2% |

| $52,528 to $82,904 | 4% |

| $82,904 to $115,084 | 6% |

| $115,084 to $145,448 | 8% |

| $145,448 to $742,958 | 9.3% |

| $742,958 to $891,542 | 10.3% |

| $891,542 to $1,000,000 | 11.3% |

| $1,000,000 to $1,485,906 | 12.3%, plus the 1% surcharge on taxable income over $1,000,000 |

| Over $1,485,906 | 13.3% effective top rate |

For married couples with one or both spouses earning high W-2 income, receiving RSUs, operating a business, or selling appreciated assets, the state tax picture can change quickly. A couple may be comfortable from a federal withholding standpoint but still underpaid for California purposes if stock vesting, business distributions, or investment sales are not modeled during the year.

2025 California Tax Brackets for Head of Household

Head of household taxpayers use a separate 2025 California tax bracket schedule that can be more favorable than single filing status when the taxpayer qualifies. Eligibility should be reviewed carefully, because the status affects brackets, deductions, estimated payments, and the planning impact of a bonus, investment sale, or other income event.

| Taxable Income | Marginal Rate |

|---|---|

| $0 to $22,167 | 1% |

| $22,167 to $52,535 | 2% |

| $52,535 to $67,721 | 4% |

| $67,721 to $83,811 | 6% |

| $83,811 to $98,997 | 8% |

| $98,997 to $505,980 | 9.3% |

| $505,980 to $607,176 | 10.3% |

| $607,176 to $1,000,000 | 11.3% |

| $1,000,000 to $1,011,960 | 12.3%, plus the 1% surcharge on taxable income over $1,000,000 |

| Over $1,011,960 | 13.3% effective top rate |

Because filing status changes the brackets, it can affect year-end projections, estimated payments, and the tax impact of discretionary income events. For taxpayers with dependents, divorce changes, or shared custody arrangements, the filing status analysis should be part of the annual tax planning process.

What Is the Mental Health Services Tax?

The Mental Health Services Tax is an additional 1% California tax on taxable income above $1 million. This surcharge is why California’s top effective personal income tax rate is commonly described as 13.3%, combining the 12.3% top regular rate with the extra 1% tax on income above the threshold.

The surcharge is especially important because the $1 million threshold can be crossed in one unusual year. A taxpayer may not normally be a top-bracket earner, but a liquidity event can change that. Common triggers include:

- Selling a business or partnership interest

- Exercising or selling startup equity

- Large RSU vesting events

- Major capital gains from investments or real estate

- Large bonuses or deferred compensation payouts

- Roth conversions or retirement account distributions

The practical takeaway is simple: any year with income approaching $1 million deserves a projection before the transaction closes or the income is recognized. Once the year ends, many planning options become limited.

What Income Is Subject to California Income Tax?

California starts with a broad view of taxable income. Residents are generally taxed on income from all sources, while nonresidents and part-year residents are taxed on California-source income. The details can become complex for people who move, work remotely, own businesses, or receive deferred compensation.

Wages and salary

California taxes wages and salary earned by residents. Nonresidents may also owe California tax on wages connected to services performed in the state. For remote workers and executives who split time between states, the sourcing analysis can be more complicated than simply looking at where the employer is located.

Business and self-employment income

Business income from sole proprietorships, partnerships, S corporations, and LLCs can be subject to California income tax. Business owners may also need to consider entity-level fees, payroll taxes, sales tax, and estimated tax payments. Clear records are essential because California tax planning often depends on the timing and character of income and deductions.

Investment income and capital gains

California generally taxes capital gains as ordinary income. Unlike the federal system, California does not offer a lower long-term capital gains rate. A long-term stock sale, cryptocurrency gain, rental property sale, or business investment gain may receive favorable federal treatment while still being taxed at California’s ordinary income tax rates.

For a deeper look at this issue, see Clear Peak Accounting’s article on California capital gains tax.

Retirement distributions

Traditional IRA distributions, 401(k) distributions, pension income, and other taxable retirement distributions are generally included in California taxable income for residents. Roth distributions may be tax-free when the federal requirements are met, but the details should be reviewed before making large retirement account decisions.

Equity compensation

RSUs, stock options, restricted stock, and deferred compensation can create California tax exposure. The state may tax income based on residency, workdays, vesting periods, and California-source rules. This is a common issue for technology professionals, startup founders, and executives who move into or out of California.

Planning a bonus, equity sale, business exit, or high-income year? Review individual tax planning options before the income is recognized.

How Do California Tax Rates Compare to Other States?

California has one of the highest personal income tax rates in the United States, with a 12.3% top regular rate and a 13.3% effective top rate after the millionaire surcharge. That makes bracket planning especially important for business owners, investors, executives, and professionals with income that changes from year to year.

That makes California very different from states with no broad wage income tax, such as Texas, Florida, Nevada, Washington, Tennessee, South Dakota, Wyoming, and Alaska. It is also different from flat-tax states where the same rate applies across most income levels.

However, a state-by-state comparison should look beyond the headline income tax rate. Property taxes, sales taxes, business taxes, local taxes, credits, deductions, and the taxpayer’s income mix can change the total picture. For business owners and high-income professionals, the most useful question is not just “What is the top rate?” It is “How will my specific income be sourced, timed, deducted, and taxed across every state involved?”

Deductions and Credits That May Reduce California Tax

California taxable income is not the same as gross income, and deductions or credits can change which tax bracket applies to part of your income. The state has its own rules, limitations, and nonconformity issues, so taxpayers should not assume that the federal result automatically produces the same California result.

Standard deduction or itemized deductions

Many taxpayers claim the California standard deduction, while others itemize. Itemized deductions may include certain mortgage interest, charitable contributions, and other eligible expenses, but California has its own limitations and adjustments. Do not assume the federal deduction result will automatically match the state result.

Retirement contributions

Contributions to traditional retirement accounts may reduce taxable income when they qualify. For business owners, retirement plan design can be one of the most powerful year-round planning tools. A solo 401(k), SEP IRA, defined benefit plan, or employer-sponsored plan may affect both current taxes and long-term cash flow.

Business deductions

Self-employed taxpayers and business owners may be able to deduct ordinary and necessary business expenses. Documentation matters. Meals, travel, home office expenses, professional fees, software, equipment, and vehicle costs should be supported by clear records and a consistent accounting process.

California credits

Credits can reduce tax dollar for dollar when a taxpayer qualifies. Depending on the situation, California credits may relate to dependents, renters, low-income taxpayers, business activities, hiring, or other state-specific programs. Credits often have detailed eligibility rules, so they should be reviewed before assuming they apply.

Business owners should also understand how federal deductions interact with California rules. For example, the qualified business income deduction is a valuable federal concept, but California does not always conform to every federal tax benefit in the same way.

Estimated Tax Payments in California

California taxpayers may need estimated tax payments when withholding is not enough to cover the expected liability. This is common for business owners, consultants, partners, real estate professionals, investors, and employees with large equity compensation or bonuses, especially when income arrives unevenly during the year.

California’s estimated payment schedule is different from the federal schedule. The state generally front-loads payments using a 30%, 40%, 0%, and 30% structure across the four payment periods. That means taxpayers cannot simply divide the annual estimate into four equal payments and assume California will treat the timing as correct.

Estimated payments are especially important when income is uneven. A founder may have little income early in the year and a large stock sale in the fourth quarter. A real estate professional may close several large transactions in one month. A physician practice owner may receive year-end distributions. In these cases, annualized income calculations and timely projections can help reduce penalty exposure.

For more detail on timing and safe harbor concepts, read Clear Peak Accounting’s article on quarterly estimated tax payments in California.

Tax Planning Strategies for High-Income Californians

High-income California taxpayers have less room for reactive planning because state tax rates can be significant and many income events are difficult to unwind. The best approach is to project early, coordinate federal and state decisions, and understand the cash flow impact before year-end.

If your California taxable income may cross a higher bracket this year, start business tax planning or contact Clear Peak Accounting before year-end decisions are locked in.

1. Model income before major transactions

Before selling a business, exercising options, selling stock, converting retirement funds, or closing a major real estate transaction, estimate the California tax impact. A projection can show the marginal rate, estimated payment need, potential surcharge exposure, and after-tax cash available.

2. Time income and deductions where possible

Some taxpayers can shift income or deductions between years. This may involve bonus timing, business expense timing, charitable giving, retirement contributions, billing cycles, or investment sales. The goal is not to force timing decisions for tax reasons alone. The goal is to understand the tradeoff before the calendar year closes.

3. Coordinate capital gains and losses

Because California taxes capital gains as ordinary income, harvesting losses, planning installment sales, and coordinating portfolio moves can matter. Capital gain planning should include federal tax, California tax, cash flow, investment risk, and the taxpayer’s broader financial plan.

4. Review entity structure

Business owners should periodically review whether their entity structure still fits their income, payroll, ownership, and growth plans. An LLC, S corporation, partnership, or C corporation can create different tax and compliance outcomes. Entity structure should be reviewed before growth, financing, sale discussions, or major compensation changes.

5. Plan for residency and sourcing before moving

Moving into or out of California can create tax issues that are easy to underestimate. Residency, domicile, stock compensation sourcing, business income sourcing, and documentation all matter. Taxpayers should plan before the move, not after receiving a state notice.

6. Keep withholding and estimates aligned

A taxpayer can have a strong income year and still face penalties if payments are late or insufficient. Review withholding and estimated tax payments after major changes, not just at tax filing time.

Common California Tax Bracket Questions

California tax bracket questions usually come down to three practical issues: the top rate, which income is taxed, and whether estimated payments are needed. The answers below are written for quick reference, but taxpayers with major income changes should still model their specific filing status, deductions, and payment timing.

What is the highest California income tax rate?

California’s top effective personal income tax rate is commonly described as 13.3%. This includes the 12.3% top regular rate plus the 1% Mental Health Services Tax on taxable income above $1 million.

Does California tax long-term capital gains at a lower rate?

No. California generally taxes long-term capital gains as ordinary income. A gain that receives a lower federal long-term capital gains rate can still be taxed at California’s regular income tax rates.

Are California tax brackets based on gross income?

No. The brackets apply to taxable income after applicable adjustments, deductions, and exemptions. Gross income is the starting point, but it is not the final number used to apply the tax rate schedule.

Do I need estimated payments if I have a salary?

Maybe. Salary withholding may be enough for some employees, but it may fall short if you also have investment gains, business income, bonuses, RSUs, rental income, or other income not fully covered by withholding.

Turn California Tax Brackets Into a Planning Tool

California tax brackets are more than a filing-season reference. They are a planning tool. When you understand how marginal rates work, which income types are taxed, when estimated payments are due, and how deductions and credits apply, you can make better decisions throughout the year.

For high-income professionals, business owners, investors, and new California residents, the biggest tax opportunities often come before the income event happens. Clear Peak Accounting helps clients move from reactive filing to proactive planning, with strategies tailored to California’s rules and each client’s financial goals.

Contact Clear Peak Accounting to schedule a conversation about California income tax planning, estimated payments, business tax strategy, or a high-income tax projection.