Qualified Business Income Deduction Explained

The qualified business income deduction can be one of the most valuable federal tax breaks for owners of pass-through businesses. If you run an S corporation, partnership, LLC, sole proprietorship, or certain real estate activity, Section 199A may allow you to deduct up to 20% of eligible business income before calculating federal income tax. The hard part is knowing when the deduction is simple, when income limits reduce it, and when professional service income creates extra restrictions.

Need help estimating your QBI deduction before year-end? Connect with Clear Peak Accounting for proactive tax planning tailored to your business structure and California filing situation.

This article explains who qualifies, how the 20% calculation works, what happens when taxable income exceeds the thresholds, why specified service trade or business rules matter, and how California business owners should plan around the fact that the state does not conform to the federal deduction.

What Is the Qualified Business Income Deduction?

The qualified business income deduction, often called the QBI deduction or Section 199A deduction, is a federal deduction for eligible owners of pass-through businesses. Pass-through income is business income that flows to the owner’s individual tax return instead of being taxed first at the corporate level.

In plain terms, the deduction can reduce the amount of business income subject to federal income tax. It does not reduce self-employment tax, payroll tax, net investment income tax, or California income tax. It also does not create a cash refund by itself if the underlying income is not taxable.

The core rule is straightforward: eligible taxpayers may be able to deduct up to 20% of qualified business income from a qualified trade or business. The final deduction can be lower because of taxable income limits, W-2 wage limits, qualified property limits, specified service business limits, and the separate cap based on taxable income after net capital gains.

For many business owners, QBI planning belongs alongside entity choice, salary planning, estimated tax payments, retirement contributions, and year-end deduction timing. Clear Peak Accounting often evaluates these issues together because a move that improves one tax item can reduce another if it is not modeled carefully. Related planning may include business tax planning, business income tax return preparation, and broader deduction strategy.

Who Qualifies for the Section 199A Deduction?

The deduction is generally available to individuals, trusts, and estates with qualified business income from a domestic trade or business. The business usually needs to be operated directly or through a pass-through structure.

Common qualifying business structures include:

- S corporations, where business income passes through on a Schedule K-1.

- Partnerships and multi-member LLCs taxed as partnerships.

- Single-member LLCs and sole proprietorships reported on Schedule C.

- Certain rental real estate enterprises that rise to the level of a trade or business or meet the rental real estate safe harbor.

- Certain trusts and estates with qualifying pass-through income.

C corporations do not qualify because they pay corporate income tax directly. W-2 wages also do not qualify, even if you are an employee-owner of your own S corporation. For S corporation owners, only the pass-through business profit may count as QBI. Reasonable compensation paid to the shareholder is not QBI.

Qualified business income is generally the net amount of qualified items of income, gain, deduction, and loss from the business. It does not include items such as capital gains or losses, dividends, interest income that is not properly allocable to the business, reasonable compensation from an S corporation, guaranteed payments from a partnership, or payments to a partner for services outside partner capacity.

How Is the 20% QBI Deduction Calculated?

At lower taxable income levels, the calculation often starts with a simple formula: qualified business income multiplied by 20%. For example, if an eligible sole proprietor has $120,000 of QBI and taxable income is below the applicable threshold, the tentative QBI deduction may be $24,000 before considering the overall taxable income cap.

The overall cap matters. The deduction generally cannot exceed 20% of taxable income minus net capital gain. This prevents taxpayers from claiming a QBI deduction against income that is not eligible business income.

A simplified calculation looks like this:

| Step | Question | Why It Matters |

|---|---|---|

| 1 | What is qualified business income? | QBI is the base for the 20% deduction. |

| 2 | What is taxable income before the QBI deduction? | Taxable income determines whether thresholds, phase-outs, and limits apply. |

| 3 | Is the business an SSTB? | Specified service businesses face stricter rules at higher income levels. |

| 4 | What are W-2 wages and qualified property? | These amounts can limit the deduction above the income threshold. |

| 5 | Does the taxable income cap reduce the result? | The final deduction is limited by taxable income after net capital gain. |

The calculation becomes more complex when you own multiple businesses, receive several Schedule K-1s, have QBI losses, hold rental real estate, or operate partly inside and partly outside a specified service field. In those cases, each activity may need to be analyzed separately before amounts are combined on the individual return.

Income Thresholds and Phase-Outs

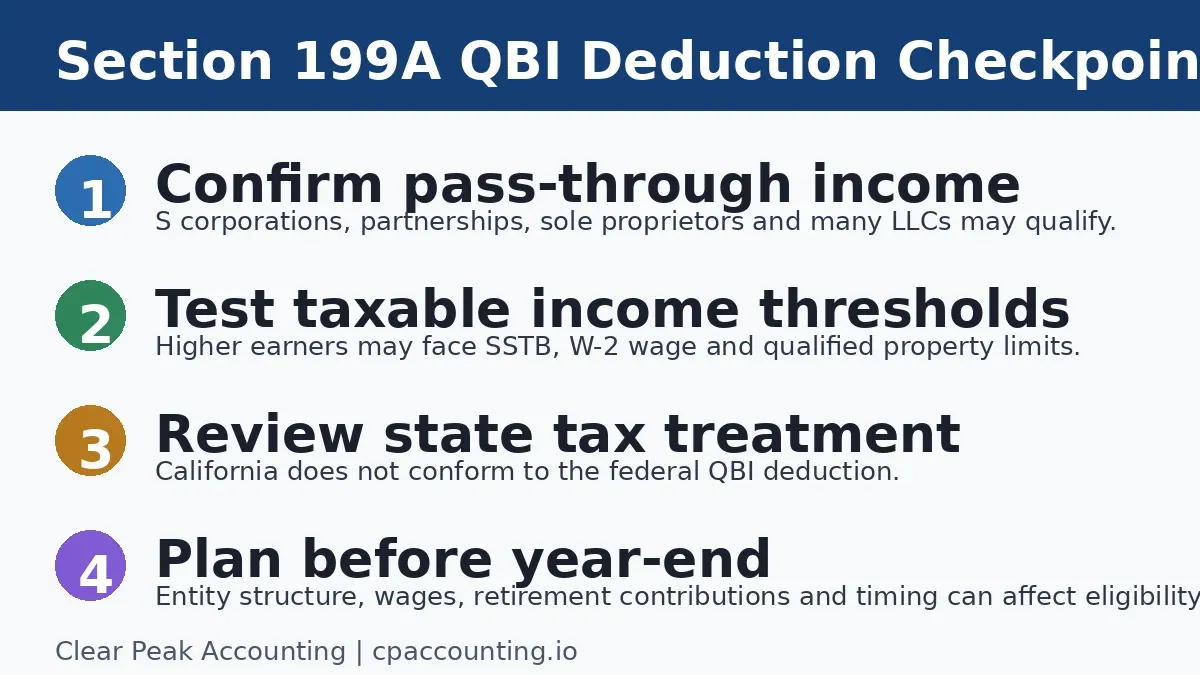

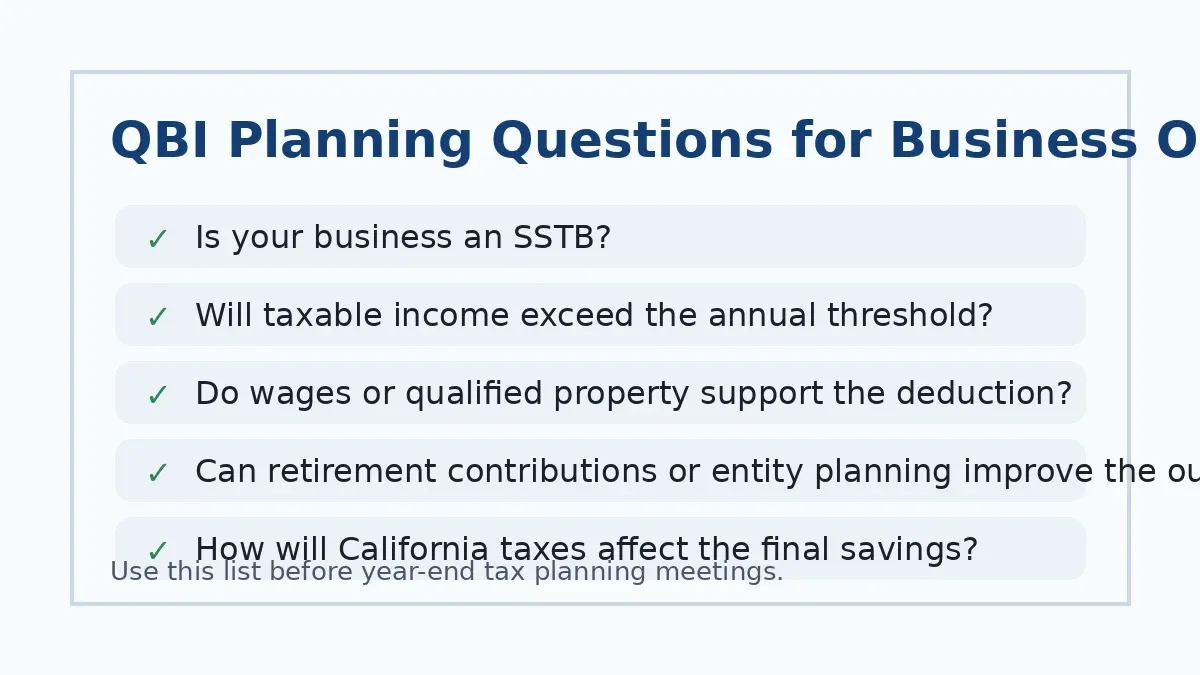

The QBI deduction is income sensitive. When taxable income is below the threshold for your filing status, many taxpayers can take the deduction without applying the W-2 wage, qualified property, or SSTB limitations. When taxable income enters the phase-out range, the limits begin to apply. Above the phase-out range, some businesses remain eligible but are limited by wage and property rules, while many specified service businesses lose the deduction entirely.

For 2025 federal returns filed in 2026, the commonly referenced taxable income thresholds are $197,300 for single filers and $394,600 for married taxpayers filing jointly, with phase-out ranges of $50,000 and $100,000, respectively. These amounts are inflation adjusted, so taxpayers should confirm the current numbers each tax year.

Taxable income is measured before the QBI deduction. That means retirement plan contributions, health savings account contributions, deductible business expenses, depreciation decisions, and timing of income can affect whether you fall below a threshold or inside the phase-out range. This is one reason year-end planning is more effective than trying to solve the issue after December 31.

Business owners should also remember that taxable income is not the same as gross receipts. A business can have high revenue but modest taxable income after payroll, operating expenses, depreciation, retirement contributions, and other deductions. Conversely, an owner with investment income, spouse wages, stock sales, or income from several businesses may exceed the QBI threshold even if one business alone looks smaller.

What Are SSTB Limitations?

An SSTB is a specified service trade or business. These are businesses where the principal asset is the reputation or skill of owners or employees in certain service fields. Examples can include health, law, accounting, actuarial science, performing arts, consulting, athletics, financial services, brokerage services, investing and investment management, trading, securities dealing, and similar fields identified under Section 199A rules.

SSTB status does not automatically eliminate the deduction. If taxable income is below the applicable threshold, SSTB owners may still qualify. The issue appears as taxable income rises. Inside the phase-out range, the available deduction is reduced. Above the phase-out range, SSTB income generally does not qualify for the QBI deduction.

For California professionals, this rule can be especially important. Physicians, dentists, consultants, attorneys, accountants, wealth advisors, content creators with personal brand income, and other high-income service professionals may see the deduction shrink or disappear as taxable income increases. A small change in taxable income can have a large effect when it moves the taxpayer into or out of the phase-out range.

Owners should be careful about aggressive attempts to separate an SSTB into a related non-service entity just to preserve the deduction. The IRS has anti-abuse rules that can treat related businesses as part of the SSTB when they provide property or services to a commonly controlled service business. Substance, documentation, and business purpose matter.

If your business is close to an income threshold, do not wait until tax filing season. Year-round business tax planning can help you evaluate retirement contributions, entity structure, salary, and deduction timing before the window closes.

W-2 Wage and Qualified Property Limits

For non-SSTB businesses above the income threshold, the deduction may be limited by W-2 wages paid by the business and the unadjusted basis immediately after acquisition of qualified property, often shortened to UBIA. This rule was designed to tie the deduction to businesses with employees or capital investment when owners have higher taxable income.

Above the threshold, the deduction is generally limited to the greater of:

- 50% of W-2 wages paid by the qualified business, or

- 25% of W-2 wages plus 2.5% of the UBIA of qualified property.

This matters for businesses that produce strong profit but pay little payroll. A sole proprietor with no employees may have a strong tentative 20% deduction at lower income levels, but the wage limitation can reduce the deduction when taxable income is high. An S corporation owner may have W-2 wages, but increasing salary only to boost QBI is not automatically beneficial because wages reduce pass-through profit and increase payroll taxes.

The qualified property component can help real estate and capital-intensive businesses. Rental real estate owners, developers, manufacturers, and businesses with significant depreciable assets should track UBIA carefully. The property rules are technical, and book depreciation schedules do not always tell the full tax story.

California Tax Treatment: Federal Benefit, State Difference

California does not conform to the federal qualified business income deduction. That means a California business owner may receive a federal deduction under Section 199A while still paying California income tax without the same reduction.

This difference affects estimated tax planning, cash flow, and how owners interpret their effective tax rate. A taxpayer may correctly reduce federal taxable income through QBI, yet still owe substantial California tax on the income. California also has its own business rules, including the annual LLC tax, gross receipts fees for certain LLCs, franchise tax considerations, payroll requirements, and state-level nonconformity issues.

For pass-through owners in Los Angeles, Santa Monica, and across California, the practical takeaway is simple: do not treat the QBI deduction as a full tax answer. It is a federal planning tool. State taxes, entity-level taxes, estimated tax payments, and California-specific compliance can change the decision. For related planning, review Clear Peak Accounting’s resources on California franchise tax and quarterly estimated tax payments in California.

Strategies to Maximize the QBI Deduction

QBI planning should be specific to your business model, filing status, income level, and long-term goals. The right strategy for a real estate investor can be very different from the right strategy for a consultant, physician, software founder, or restaurant owner.

Manage taxable income before year-end

Because thresholds are based on taxable income before the QBI deduction, reducing taxable income can preserve or increase the deduction. Common planning tools include retirement plan contributions, health savings account contributions, accountable plan reimbursements, timing of equipment purchases, and accelerating legitimate business expenses when appropriate. See Clear Peak Accounting’s article on small business tax deductions for additional deduction categories to review.

Evaluate S corporation compensation carefully

S corporation shareholder wages do not count as QBI, but they can affect the W-2 wage limitation. A reasonable salary is required, and the best answer is not always the lowest possible salary. The planning question is how salary, payroll tax, QBI, retirement contributions, and reasonable compensation standards work together.

Consider retirement plan design

A SEP IRA, Solo 401(k), cash balance plan, or employer retirement plan may reduce taxable income enough to improve QBI eligibility. The benefit should be modeled because retirement contributions can also reduce business income in some contexts. The goal is not simply to chase the deduction, but to improve after-tax cash flow and long-term wealth planning.

Track separate activities and losses

QBI losses generally carry forward and reduce future QBI. Owners with multiple businesses should track income and losses by activity. A loss from one pass-through activity can reduce the combined QBI deduction from profitable activities.

Analyze whether aggregation is allowed

Some owners can aggregate qualified businesses for QBI purposes if specific requirements are met. Aggregation may help when one business has wages or property and another has income. It also creates consistency obligations. The election should be made only after reviewing ownership, services, products, and operational connections.

Common Mistakes Business Owners Make

- Assuming all LLC income qualifies. Entity type alone does not determine eligibility. The income must be qualified business income from a qualified trade or business.

- Ignoring SSTB status. High-income service professionals can lose the deduction if taxable income exceeds the phase-out range.

- Forgetting the California difference. The deduction may reduce federal tax but not California tax.

- Using gross revenue instead of taxable income. Thresholds are based on taxable income before QBI, not sales.

- Setting S corporation salary without modeling. Salary affects reasonable compensation, payroll tax, retirement contributions, pass-through income, and wage limitations.

- Waiting until return preparation. Many QBI strategies require action before year-end.

FAQ About the Qualified Business Income Deduction

Does the QBI deduction reduce self-employment tax?

No. The QBI deduction reduces federal taxable income for income tax purposes. It does not reduce self-employment tax, payroll tax, or California income tax.

Can rental real estate qualify for QBI?

Sometimes. Rental real estate may qualify if it rises to the level of a trade or business or meets the IRS rental real estate safe harbor. Owners should document hours, services, separate books, and the business nature of the activity.

Do S corporation wages count as QBI?

No. Reasonable compensation paid to an S corporation shareholder is not QBI. The pass-through profit reported to the owner may qualify if other requirements are met.

Is the QBI deduction available for California state tax?

No. California does not conform to the federal Section 199A deduction, so the benefit is federal only for California taxpayers.

Should I change entity type just for the QBI deduction?

Usually not without a broader tax analysis. Entity choice affects payroll tax, legal structure, administrative cost, retirement planning, California taxes, and future exit planning. QBI is only one part of the decision.

Plan Before the Deduction Becomes a Filing-Season Surprise

The qualified business income deduction can create meaningful federal tax savings, but it is not automatic for every pass-through owner. The result depends on your business type, taxable income, SSTB status, wages, property, losses, filing status, and California tax picture.

For business owners, the best time to review QBI is before year-end, when there is still time to adjust taxable income, evaluate retirement contributions, review S corporation salary, document rental real estate activity, and coordinate federal planning with California compliance.

Clear Peak Accounting helps California business owners move beyond reactive tax filing into proactive planning. Start a conversation about your QBI deduction, entity structure, and year-round tax strategy.