Choosing between cash and accrual accounting is one of the first financial decisions every small business owner faces. The method you pick affects how you track revenue and expenses, when you pay taxes, and how clearly you can see your company’s financial health. For many California business owners, this choice has real consequences for cash flow, tax planning, and growth strategy.

This article breaks down cash vs accrual accounting in plain language, walks through real-world examples, and covers everything from IRS requirements to switching methods, so you can make a confident, informed decision for your business.

What Is Cash Basis Accounting?

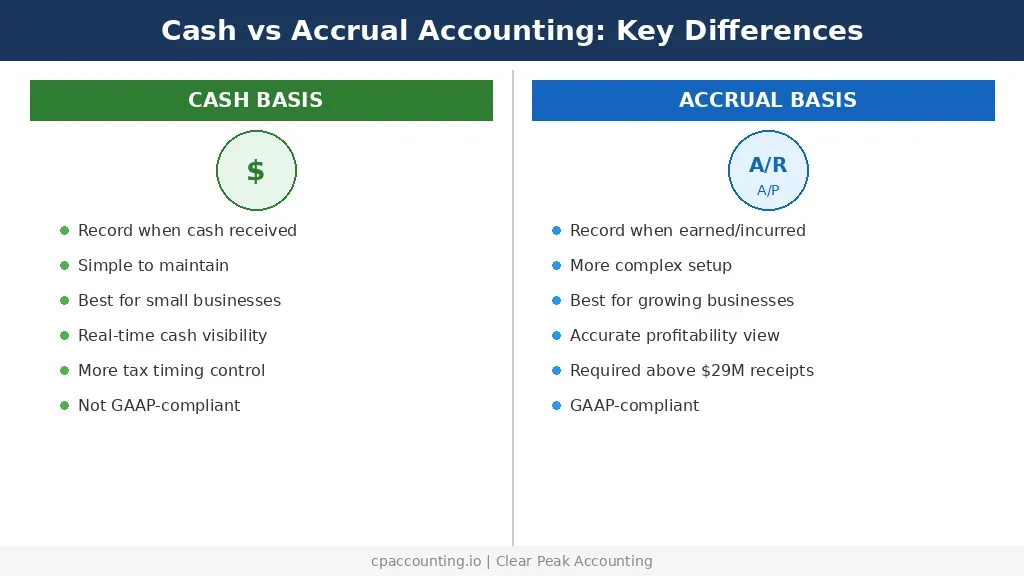

Cash basis accounting records revenue when you actually receive payment and records expenses when you actually pay them. It follows the money: if cash hasn’t changed hands, the transaction doesn’t appear on your books yet.

How it works in practice: Suppose you complete a consulting project on March 15 and send your client a $5,000 invoice. The client pays on April 10. Under cash basis accounting, you record that $5,000 as income in April, when the payment hit your bank account, not in March when the work was done.

The same logic applies to expenses. If you receive a $1,200 bill for office supplies in June but pay it in July, you record the expense in July.

Who Uses Cash Basis Accounting?

Cash basis accounting is the most common method among sole proprietors, freelancers, and small businesses with straightforward transactions. It’s popular because it’s simple to maintain and gives you a clear picture of how much actual cash you have at any given time.

What Is Accrual Basis Accounting?

Accrual basis accounting records revenue when it’s earned and expenses when they’re incurred, regardless of when money actually changes hands. This method matches income with the expenses that generated it, providing a more complete picture of your business’s financial performance over any given period.

How it works in practice: Using the same consulting example, under accrual accounting you would record the $5,000 as revenue in March, when you completed the project and earned the right to payment. The fact that the client hasn’t paid yet doesn’t change the accounting. You’d also record the office supply expense in June when you received the goods, not in July when you paid.

Who Uses Accrual Basis Accounting?

Accrual accounting is used by larger businesses, companies that carry inventory, and any business that wants financial statements aligned with Generally Accepted Accounting Principles (GAAP). If you’re seeking investors, applying for significant loans, or planning for rapid growth, accrual accounting gives stakeholders a more reliable view of your financial position.

Cash vs Accrual Accounting: Side-by-Side Comparison

The table below summarizes the key differences between cash and accrual accounting methods across the factors that matter most to small business owners.

| Factor | Cash Basis | Accrual Basis |

|---|---|---|

| When revenue is recorded | When payment is received | When revenue is earned |

| When expenses are recorded | When payment is made | When expense is incurred |

| Complexity | Simple to set up and maintain | More complex; often requires professional help |

| Cash flow visibility | Excellent; reflects actual cash on hand | Less intuitive; profit doesn’t always equal cash |

| Financial accuracy | Can distort profitability in any given period | More accurate picture of true financial performance |

| GAAP compliance | Not GAAP-compliant | GAAP-compliant |

| Tax timing | Pay taxes when income is received | Pay taxes when income is earned (even if unpaid) |

| Best for | Small businesses, freelancers, sole proprietors | Growing businesses, inventory-based, investor-backed |

| IRS requirement | Available to most small businesses | Required for businesses with >$29M gross receipts |

IRS Rules: When You Must Use Accrual Accounting

The IRS gives most small businesses the freedom to choose either method, but there are situations where accrual accounting becomes mandatory.

The Gross Receipts Test

Under the Tax Cuts and Jobs Act (TCJA), businesses with average annual gross receipts of $29 million or more (over the prior three tax years) are generally required to use the accrual method. This threshold is indexed for inflation, so it adjusts slightly each year. Businesses under this threshold can typically use either method.

C Corporations and Tax Shelters

C corporations that exceed the gross receipts threshold must use accrual accounting. However, C corporations that meet the small business gross receipts test can still use the cash method. Tax shelters are always required to use the accrual method, regardless of size.

Inventory-Based Businesses

Historically, any business that maintained inventory was required to use accrual accounting. The TCJA relaxed this rule significantly. Now, businesses that meet the $29 million gross receipts test can use the cash method even if they carry inventory. If you’re a small retailer or e-commerce seller below this threshold, you likely have the flexibility to choose.

Partnerships and S Corporations

Partnerships and S corporations that have a C corporation as a partner or shareholder may face additional restrictions. However, most small partnerships and S corps with receipts under the threshold can still elect cash basis.

How Each Method Affects Your Taxes

Your accounting method directly impacts when you owe taxes, which affects your tax planning strategy. Understanding the tax timing differences is essential for managing cash flow effectively.

Cash Basis Tax Timing

With the cash method, you only pay taxes on money you’ve actually received. This creates opportunities for strategic timing:

- Defer income: If you’re approaching year-end, you can delay sending invoices until January to push that income into the next tax year.

- Accelerate expenses: Paying bills, buying supplies, or prepaying certain expenses before December 31 reduces your current-year taxable income.

- Predictable tax bills: Since you only pay tax on cash received, your tax obligation more closely matches your ability to pay.

Accrual Basis Tax Timing

With the accrual method, you owe taxes on income you’ve earned but may not have collected yet. This can create cash flow challenges:

- Tax on uncollected revenue: If a client owes you $20,000 at year-end but hasn’t paid, you still owe taxes on that amount.

- Expense matching benefits: You can deduct expenses when incurred, even if you haven’t paid the bill yet, which can offset some of the timing disadvantage.

- Better long-term planning: Accrual accounting smooths out income and expense fluctuations, making year-over-year tax projections more accurate.

For small business owners with seasonal revenue patterns or irregular cash flow, the differences in tax timing between these methods can mean thousands of dollars in earlier or later tax payments. A proactive tax savings strategy can help you navigate these timing differences.

Pros and Cons of Cash Basis Accounting

Advantages

- Simplicity: Easier to learn, implement, and maintain. Many business owners can handle it themselves with basic accounting software.

- Real-time cash visibility: Your books always reflect how much money you actually have, making it easier to manage day-to-day operations.

- Tax timing control: You have more flexibility to time income and expenses for tax advantages.

- Lower accounting costs: Simpler records typically mean lower bookkeeping and accounting fees.

Disadvantages

- Misleading profitability: If you receive a large payment one month and none the next, your financials will show dramatic swings that don’t reflect actual business performance.

- Not GAAP-compliant: Investors, banks, and some partners may require GAAP-compliant financials, which means accrual.

- Harder to plan long-term: Without matching revenue to the expenses that generated it, it’s difficult to evaluate the true cost and profitability of projects or products.

- Limited scalability: As your business grows and transactions become more complex, cash basis may not provide the financial clarity you need.

Pros and Cons of Accrual Basis Accounting

Advantages

- Accurate financial picture: Matching revenue with related expenses gives a true view of profitability for any period.

- GAAP compliance: Required by investors, lenders, and many regulatory bodies. Essential if you plan to seek outside funding.

- Better forecasting: With monthly financial statements based on accrual data, you can forecast revenue, manage budgets, and plan growth more reliably.

- Tracks receivables and payables: You always know what’s owed to you and what you owe, giving you better control over your financial obligations.

Disadvantages

- Cash flow blind spots: You might show strong profits on paper while struggling to cover payroll because clients haven’t paid yet.

- Higher complexity: Requires tracking accounts receivable, accounts payable, deferred revenue, and other accrual entries. Most businesses need professional accounting support.

- Tax on unreceived income: You may owe taxes on revenue you haven’t collected, which can strain cash flow.

- Higher accounting costs: The complexity usually means higher fees for bookkeeping and tax preparation.

Which Method Is Best for Your Business Type?

The right choice depends on your business size, industry, growth plans, and how you use financial data to make decisions. Here’s a practical breakdown:

Cash Basis Is Usually Better If You:

- Are a freelancer, sole proprietor, or single-member LLC

- Have annual gross receipts well under $29 million

- Don’t carry significant inventory

- Want the simplest possible bookkeeping system

- Primarily need to track actual cash flow

- Don’t plan to seek venture capital or large bank loans in the near term

Accrual Basis Is Usually Better If You:

- Have or plan to seek investors or significant financing

- Carry inventory as a core part of your business

- Have annual gross receipts approaching or exceeding $29 million

- Need GAAP-compliant financials for stakeholders

- Want a more accurate view of profitability per project or period

- Operate a subscription-based, SaaS, or recurring revenue model

Industry-Specific Considerations

Technology startups: If you’re a startup seeking investment, investors will almost certainly require accrual-based financials. Start with accrual from day one to avoid a costly conversion later.

Real estate professionals: Real estate agents and brokers with irregular commission income often benefit from cash basis for its simplicity and tax timing advantages.

Healthcare practices: Medical, dental, and therapy practices that bill insurance companies often find accrual more useful since there’s typically a significant gap between performing services and receiving payment.

Professional services: Consultants, attorneys, and marketing agencies may start with cash basis and switch to accrual as they grow and take on longer-term contracts.

How to Switch from Cash to Accrual Accounting (or Vice Versa)

If your business circumstances change, you can switch accounting methods. Here’s what the process involves:

- Determine eligibility. Most small businesses can switch methods, but you need IRS approval. The IRS generally allows the change as long as you follow the correct process.

- File IRS Form 3115. To change your accounting method, you must file Form 3115, Application for Change in Accounting Method. This form is filed with your tax return for the year you want the change to take effect. It calculates a “Section 481(a) adjustment,” which accounts for income or expenses that would otherwise be counted twice or not at all during the transition.

- Calculate the Section 481(a) adjustment. When switching from cash to accrual, you’ll typically have a positive adjustment (additional taxable income) because you must now recognize accounts receivable that weren’t previously on your books. When switching from accrual to cash, the adjustment is usually negative (reducing taxable income). The IRS allows you to spread a positive adjustment over four years to soften the tax impact.

- Update your systems. Work with your accountant to update your accounting software and processes. This includes adjusting opening balances, setting up new accounts (like accounts receivable and accounts payable if moving to accrual), and training your team on the new recording procedures.

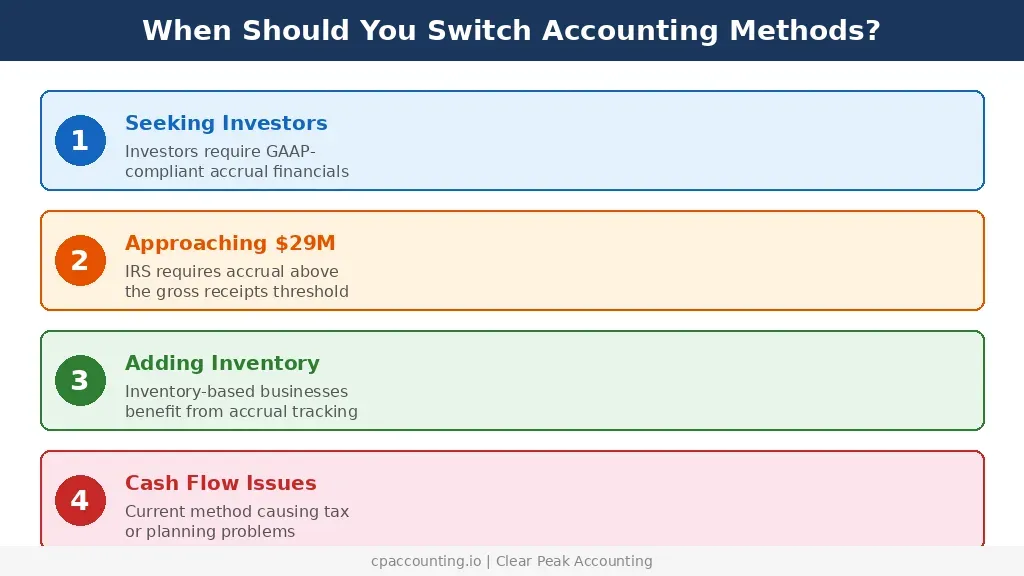

When Should You Consider Switching?

- You’re raising outside capital and investors need GAAP financials

- You’ve crossed or are approaching the $29 million gross receipts threshold

- Your business model has changed significantly (e.g., you now carry inventory)

- Your current method is causing cash flow or tax planning problems

- You’re merging with or acquiring a business that uses a different method

Modified Cash Basis: A Middle Ground

Some businesses use a modified cash basis (also called the hybrid method), which combines elements of both approaches. Under this method, you might use cash basis for most transactions but record certain items, like long-term assets or debt, on an accrual basis.

The modified cash method offers more detail than pure cash basis while remaining simpler than full accrual. However, it’s not GAAP-compliant, and you’ll need to ensure your specific combination of methods is acceptable to the IRS.

Common Mistakes to Avoid

When choosing and implementing an accounting method, watch out for these frequent pitfalls:

- Mixing methods without awareness: Some business owners unintentionally use elements of both methods, which can create tax compliance issues and inaccurate financials.

- Choosing based on this year’s taxes alone: The cheapest option for this year’s tax bill isn’t always the best long-term strategy. Consider your three-to-five year business plan.

- Ignoring the switch cost: Converting from one method to another involves accounting fees, system changes, and the Section 481(a) adjustment. Factor these costs into your decision.

- Not matching method to business model: A subscription SaaS company on cash basis will have wildly misleading financials. Match your method to how your business actually generates and recognizes revenue.

- Forgetting state requirements: California generally conforms to federal rules on accounting methods, but some states have nuances. Verify that your chosen method meets both federal and state requirements.

Frequently Asked Questions

Can I use cash basis if I have employees?

Yes. Having employees does not disqualify you from using cash basis accounting. The determining factors are your gross receipts, business structure, and whether you carry inventory (for businesses above the $29 million threshold).

Do I need to tell the IRS which method I use?

You declare your accounting method on your first tax return by filing with that method. Once established, you need IRS permission (via Form 3115) to change it.

What accounting method do most small businesses use?

The majority of small businesses use cash basis accounting because of its simplicity. Cash basis is the most common method for businesses with under $1 million in gross receipts.

Can I use different methods for different purposes?

You must use one method for tax reporting. However, you can maintain internal management reports using a different method. Many businesses file taxes on cash basis but run accrual-based internal reports for strategic decision-making.

How does my accounting method affect getting a business loan?

Many banks and lenders prefer or require accrual-based financial statements because they provide a more complete picture of your financial obligations and expected revenue. If you use cash basis, a lender may ask you to prepare accrual-adjusted financials as part of the loan application.

Make the Right Choice for Your Business

The decision between cash and accrual accounting isn’t just an administrative detail. It shapes how you see your business, plan your taxes, and present your finances to lenders and investors. For many small businesses, cash basis offers the simplicity and tax flexibility that makes the most sense early on. As your company grows, accrual accounting becomes increasingly valuable for strategic planning and stakeholder confidence.

For related guidance from Clear Peak Accounting, see our resources on marketing agency accounting support.

If you’re unsure which method fits your situation, or if you’re considering a switch, schedule a consultation with Clear Peak Accounting. Our team helps California business owners across every industry we serve choose and implement the right accounting foundation for sustainable growth.