If you own an LLC, S Corp, or C Corp in California, the California franchise tax is one of those recurring obligations you cannot ignore. It applies regardless of whether your business turns a profit, and failing to pay it can lead to your entity being suspended by the state.

This article breaks down exactly what the California franchise tax is, how it differs from income tax, how much each entity type owes, when payments are due, and what happens if you fall behind.

What Is the California Franchise Tax?

The California franchise tax is a fee that the state charges business entities for the privilege of operating in California. It is administered by the California Franchise Tax Board (FTB), which is the state agency responsible for collecting both personal and business income taxes.

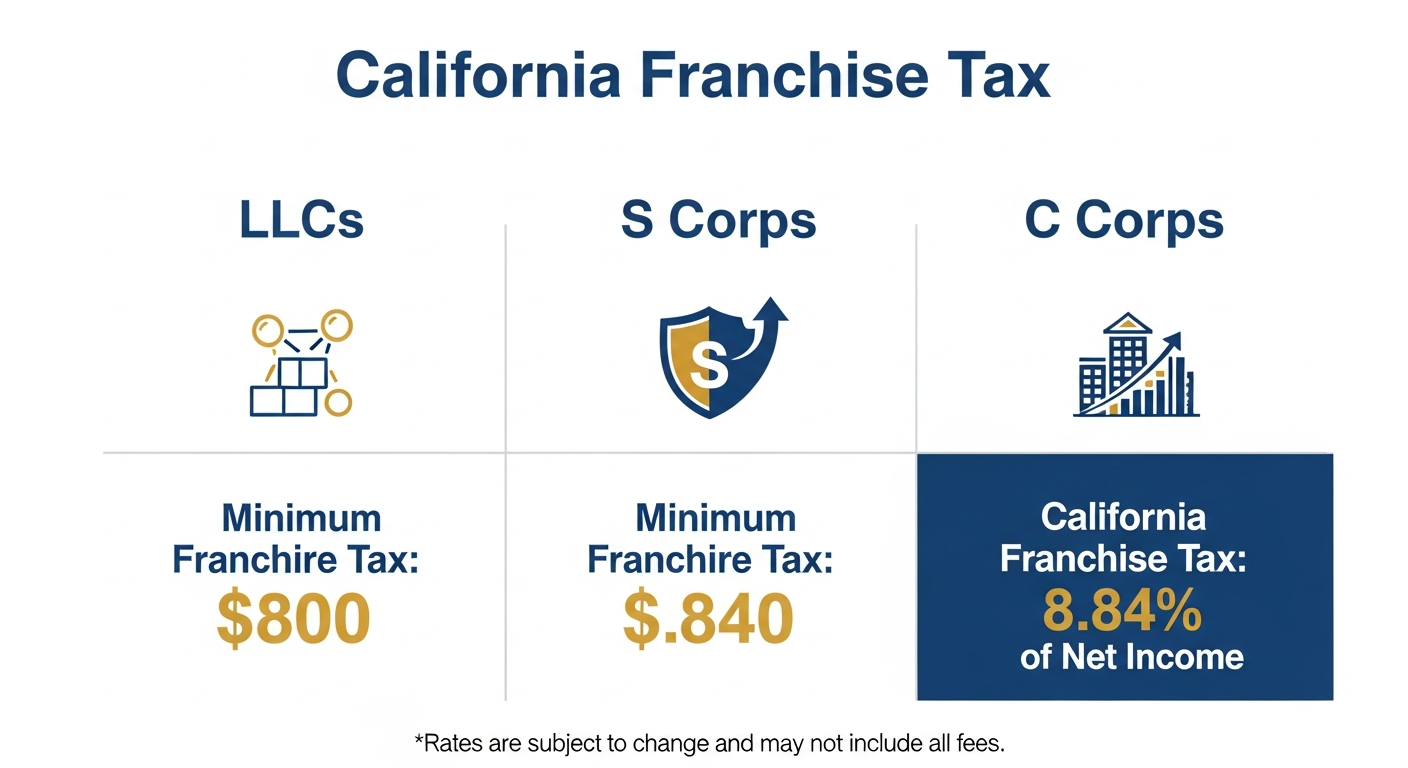

Unlike income tax, which is based on how much your business earns, the franchise tax includes a minimum payment of $800 per year that every qualifying entity must pay, even if the business had zero revenue, operated at a loss, or was completely inactive for the year.

The following entity types are subject to the California franchise tax:

- C Corporations

- S Corporations

- Limited Liability Companies (LLCs)

- Limited Partnerships (LPs)

- Limited Liability Partnerships (LLPs)

If your business is incorporated in California, registered with the Secretary of State, or simply conducting business in the state, this tax applies to you.

Franchise Tax vs. Income Tax: What Is the Difference?

Many California business owners confuse the franchise tax with income tax, but they are distinct obligations.

| Franchise Tax | Income Tax | |

|---|---|---|

| What it covers | The right to operate as a business entity in California | Tax on net earnings or profits |

| Minimum payment | $800 per year (regardless of income) | Based on actual income; could be $0 |

| Who administers it | California Franchise Tax Board (FTB) | California Franchise Tax Board (FTB) |

| Applies when inactive? | Yes | No (if no income) |

In practice, your total tax bill to the FTB often combines both. For example, a C Corp pays the greater of the $800 minimum franchise tax or 8.84% of its net income. The franchise tax sets the floor; the income-based tax determines whether you owe more.

How Much Is the California Franchise Tax by Entity Type?

The amount you owe depends on your business structure. Here is a breakdown for each entity type.

C Corporations

C Corps pay the greater of:

- $800 minimum franchise tax, or

- 8.84% of net taxable income

For example, a C Corp with $100,000 in California net income would owe $8,840 (8.84% × $100,000), since that exceeds the $800 minimum.

C Corps file Form 100 with the FTB.

S Corporations

S Corps pay the greater of:

- $800 minimum franchise tax, or

- 1.5% of net income

Financial S Corps pay a higher rate of 3.5%.

An S Corp with $200,000 in net income would owe $3,000 (1.5% × $200,000). Because income passes through to shareholders, the owners also report their share on personal state returns.

S Corps file Form 100S with the FTB.

LLCs (Limited Liability Companies)

LLCs face a two-part obligation:

- $800 annual tax (no exceptions for LLCs formed after January 1, 2024)

- Gross receipts fee based on total California income:

| Total California Income | LLC Fee |

|---|---|

| $250,000 – $499,999 | $900 |

| $500,000 – $999,999 | $2,500 |

| $1,000,000 – $4,999,999 | $6,000 |

| $5,000,000 or more | $11,790 |

An LLC earning $600,000 in California would pay $800 (annual tax) + $2,500 (gross receipts fee) = $3,300 total.

LLCs file Form 568 and pay the annual tax using Form FTB 3522.

First-Year Exemption: Who Qualifies?

Newly incorporated or qualified corporations (C Corps and S Corps) are not required to pay the minimum franchise tax in their first taxable year, for taxable years beginning on or after January 1, 2020.

However, LLCs do not qualify for a first-year exemption. A temporary exemption existed for LLCs formed between January 1, 2021, and January 1, 2024 (under Assembly Bill 85), but that program has expired. As of 2024, every LLC organized or doing business in California must pay the $800 annual tax from year one.

Corporations are also exempt from the minimum tax if:

- The taxable year was 15 days or fewer, and

- They did not conduct any business in California during that period

When Is the California Franchise Tax Due?

Due dates vary by entity type:

| Entity Type | Due Date | Form |

|---|---|---|

| C Corporation | 15th day of the 4th month after the close of the taxable year (typically April 15) | Form 100 |

| S Corporation | 15th day of the 3rd month after the close of the taxable year (typically March 15) | Form 100S |

| LLC | 15th day of the 4th month after the beginning of the taxable year (typically April 15) | FTB 3522 |

S Corps get an automatic 6-month extension to file (not to pay). C Corps get an automatic 7-month extension to file. The payment itself is still due on the original deadline.

How to Pay the California Franchise Tax

The California Franchise Tax Board offers several payment methods:

- Web Pay at ftb.ca.gov (most common for electronic payments)

- Electronic funds withdrawal when e-filing

- Mail with the applicable payment voucher (Form FTB 3586 for corps, Form FTB 3522 for LLCs)

- Credit card through approved third-party processors

Estimated tax payments are required for corporations and LLCs that expect to owe more than the $800 minimum. The standard estimated payment schedule for corporations splits across three quarters: 30% in Q1, 40% in Q2, and 30% in Q4.

What Happens If You Do Not Pay?

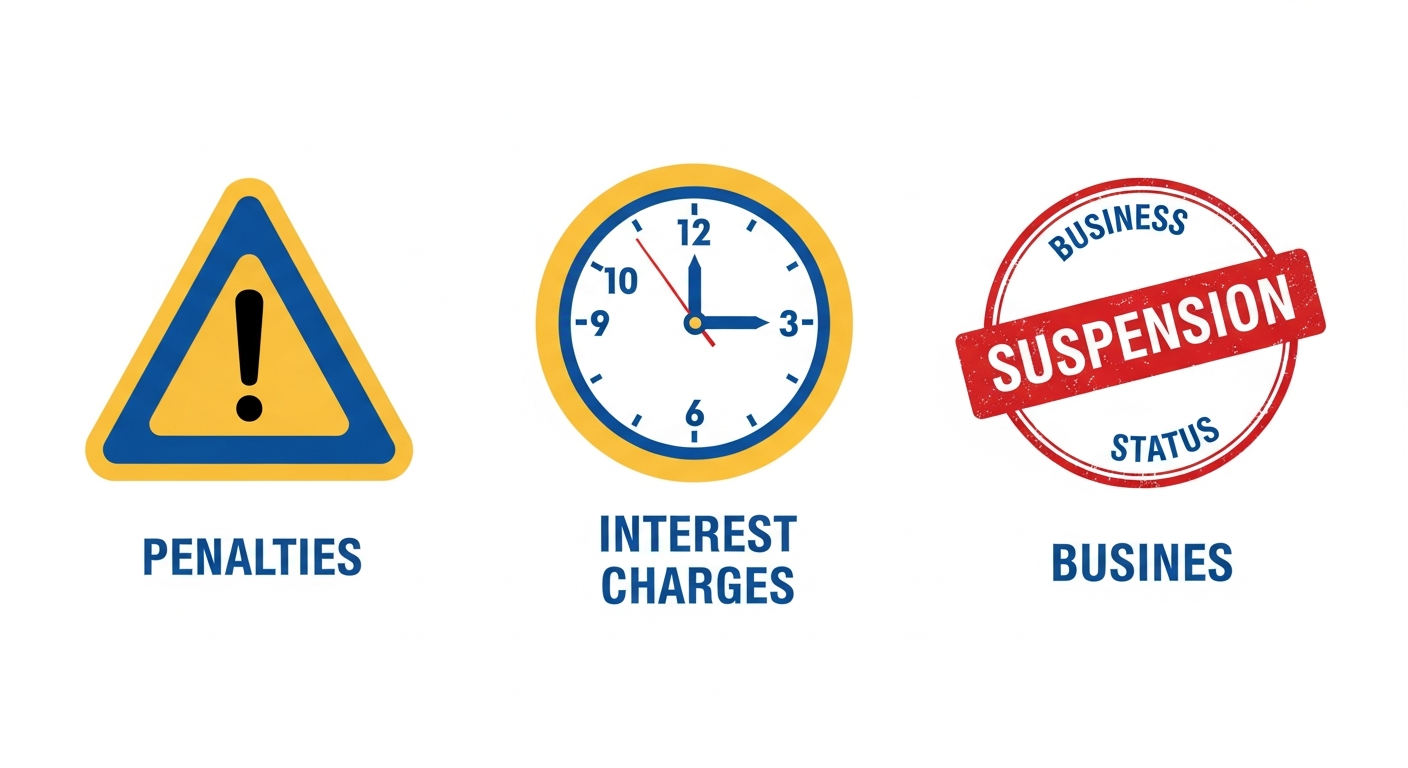

Ignoring the California franchise tax has serious consequences:

- Late payment penalty: 5% of the unpaid tax, plus an additional 0.5% for each month the balance remains unpaid

- Interest: Accrues on all unpaid amounts until fully paid

- Suspension or forfeiture: The FTB can suspend your business entity, which means you lose the right to conduct business, file lawsuits, or defend lawsuits in California. Your entity name is also no longer protected.

Reinstatement after suspension requires paying all back taxes, penalties, interest, and filing all delinquent returns. The Secretary of State also charges a $250 penalty for failure to file the Statement of Information.

Pass-Through Entity Elective Tax: An Additional Consideration

California offers a Pass-Through Entity (PTE) elective tax under AB 150 that allows S Corps and partnerships to pay state income tax at the entity level. This creates a workaround for the federal $10,000 SALT deduction cap, since the entity-level tax payment is deductible as a business expense.

This election is available to S Corps and partnerships but not C Corps. It is separate from the franchise tax and does not replace the $800 minimum. If you are considering this election, work with a qualified CPA to evaluate whether it makes sense for your situation.

Frequently Asked Questions

What is the California Franchise Tax Board?

The California Franchise Tax Board (FTB) is the state agency that administers California’s personal and business income tax laws. It collects the franchise tax, processes returns, issues refunds, and enforces tax compliance for all business entities operating in the state.

Do I have to pay the franchise tax if my business is inactive?

Yes. The $800 minimum franchise tax applies even if your business is inactive, has no income, or operates at a loss. The only way to stop the annual obligation is to formally dissolve, surrender, or cancel your entity with both the FTB and the Secretary of State.

Is the California franchise tax deductible?

The franchise tax is generally deductible as a business expense on your federal tax return. However, California does not allow a deduction for the franchise tax paid to itself. Consult with a tax professional to confirm how it applies to your specific situation.

What is the difference between the LLC annual tax and the LLC fee?

The $800 annual tax is a flat amount that every California LLC must pay. The LLC fee is an additional charge based on your total California gross receipts, starting at $900 for income over $250,000. Both are owed to the FTB, and both are due annually.

Stay on Top of Your California Franchise Tax Obligations

The California franchise tax is a non-negotiable cost of doing business in the state. Whether you operate as an LLC, S Corp, or C Corp, understanding your obligations, deadlines, and payment options helps you avoid unnecessary penalties and keep your entity in good standing.

If you need help with business tax planning or entity formation and maintenance, Clear Peak Accounting works with California small business owners across technology, real estate, healthcare, and professional services. Our fixed-fee pricing means no surprises.

Contact us to discuss your franchise tax situation.