S-Corp vs LLC California Taxes: Which Entity Saves More?

Choosing between an S-Corp and LLC in California is not just a legal decision. It affects how you pay yourself, how much self-employment tax you owe, what California charges your business each year, and how much compliance work lands on your calendar. For many profitable service businesses, the S-Corp vs LLC California taxes question comes down to whether payroll-based tax savings are large enough to outweigh the extra cost and structure.

Short answer: An LLC is often simpler and less expensive at lower profit levels. An S-Corp may save money once the business earns enough profit to pay the owner a reasonable W-2 salary and still leave meaningful distributions. The right answer depends on profit, payroll needs, California fees, owner compensation, ownership plans, and the cost of maintaining clean records.

That last point matters. A structure that looks efficient on paper can become expensive if payroll is late, bookkeeping is not current, or the owner salary is not defensible. Clear Peak Accounting helps California business owners compare the tax savings, compliance requirements, and cash flow impact before making the election.

S-Corp vs LLC in California: Quick Comparison

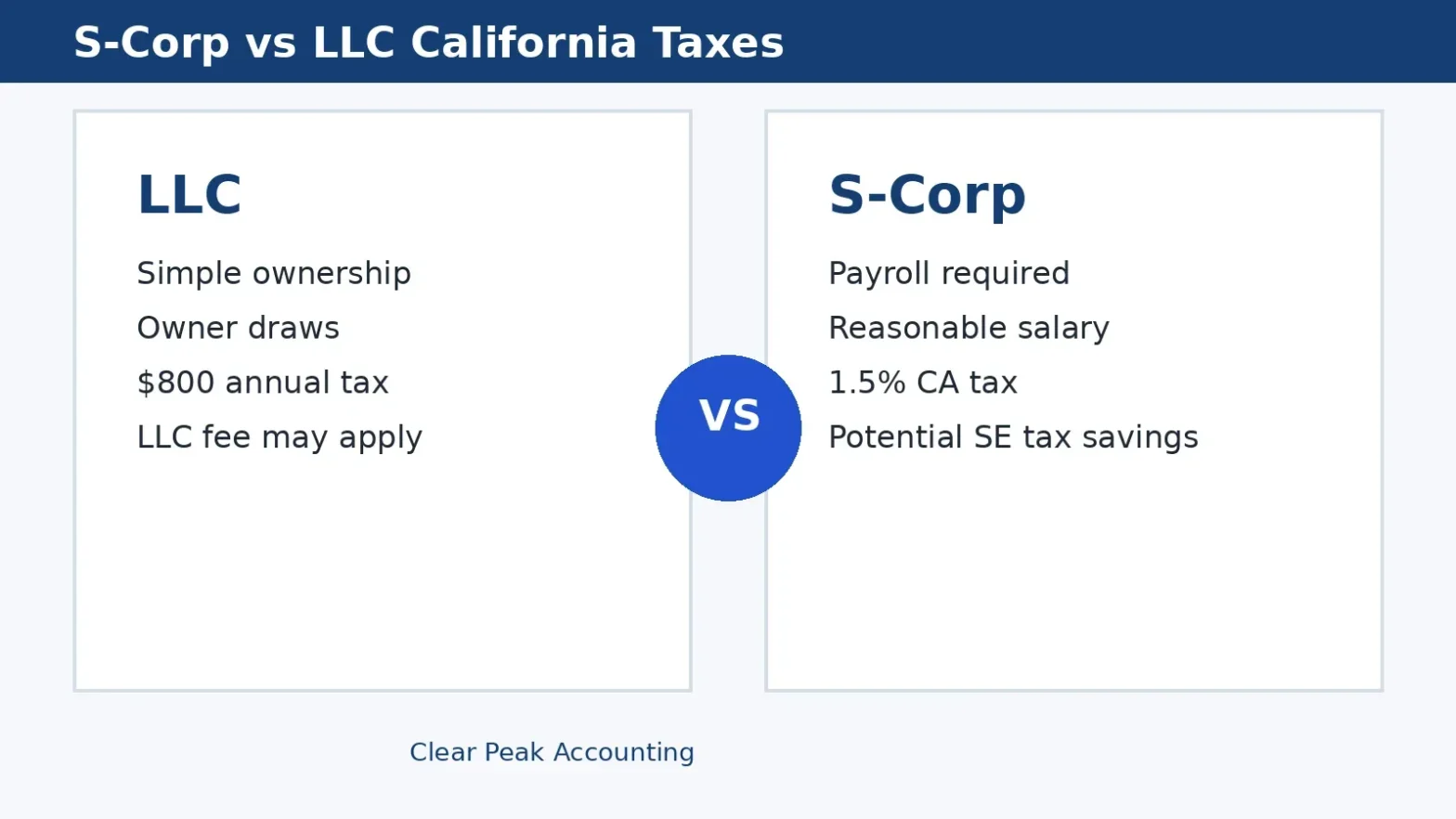

Before looking at numbers, separate the federal tax issue from the California tax issue. LLCs are legal entities that can be taxed in different ways. An S-Corp is a federal tax election available to eligible corporations and LLCs. In practice, many California business owners form an LLC, then elect S-Corp tax treatment once the business becomes profitable enough.

| Factor | LLC Taxed as Disregarded Entity or Partnership | S-Corp Tax Treatment |

|---|---|---|

| Owner pay | Owner draws or member distributions | Reasonable W-2 salary plus shareholder distributions |

| Self-employment tax | Generally applies to active owner business income | Applies to salary through payroll taxes, but not S-Corp distributions |

| California minimum tax | $800 annual LLC tax for most California LLCs | 1.5% California tax on net income, with an $800 minimum for most S-Corps |

| Additional California fee | LLC fee may apply once California total income exceeds $250,000 | No California LLC gross receipts fee after valid S-Corp treatment |

| Compliance | Simpler bookkeeping and owner payments | Payroll, reasonable compensation support, corporate formalities, Form 1120-S, K-1s |

| Best fit | Early-stage, lower profit, simple ownership, flexible operations | Consistently profitable businesses where payroll tax savings exceed added costs |

How an LLC Is Taxed in California

A single-member LLC is usually treated as a disregarded entity for federal tax purposes, while a multi-member LLC is typically treated as a partnership unless it makes another election. For an active business owner, that usually means business profit flows through to the owner and may be subject to self-employment tax.

California adds its own layer. According to the California Franchise Tax Board, every LLC doing business or organized in California generally owes an $800 annual tax. California LLCs may also owe an additional fee when total California income exceeds $250,000. That fee is separate from income tax and can matter for growing businesses with higher gross receipts.

For a deeper look at the mechanics, Clear Peak Accounting has a separate article on the California franchise tax. This article focuses on the strategic choice between LLC and S-Corp treatment, not just the filing rules.

How an S-Corp Is Taxed in California

An S-Corp generally passes income through to shareholders for federal income tax purposes. The major planning opportunity is compensation. An owner-employee must be paid a reasonable W-2 salary for the work they perform. Payroll taxes apply to that salary. Remaining profit may be distributed as S-Corp distributions, which are generally not subject to self-employment tax.

That is the reason S-Corp planning can create savings. If a profitable business owner can support a reasonable salary of $90,000 and the business still has $60,000 of profit available for distributions, the distribution portion may avoid self-employment tax. But the IRS expects the salary to be reasonable based on duties, industry, time spent, experience, and comparable compensation. Setting an artificially low salary is a red flag.

California S-Corps also pay state-level entity tax. California generally taxes S-Corporations at 1.5% of net income, with an $800 minimum for many entities. That means the S-Corp is not automatically cheaper at the state level. The analysis has to compare federal payroll tax savings against California S-Corp tax, payroll costs, bookkeeping costs, and tax preparation costs.

Worked Example: When an S-Corp Can Save Money

Assume a California consulting business earns $180,000 in net profit before owner compensation. The owner is actively working in the business. This simplified example ignores income tax brackets, deductions, retirement plan design, and other variables, so it should be treated as a planning illustration rather than a final tax projection.

| Item | LLC | S-Corp |

|---|---|---|

| Business profit before owner pay | $180,000 | $180,000 |

| Reasonable owner salary | Not required | $95,000 |

| Potential distribution after salary | Not applicable | $85,000 before entity tax and expenses |

| Federal self-employment or payroll tax exposure | Broadly applies to active owner profit | Payroll taxes apply to salary, not the distribution portion |

| California entity cost | $800 annual LLC tax, plus any applicable LLC fee | 1.5% S-Corp tax on net income, with $800 minimum |

| Added compliance cost | Lower | Payroll, bookkeeping, S-Corp return, reasonable salary documentation |

If the S-Corp distribution portion is $85,000, the potential payroll tax savings could be meaningful. At the same time, the business may add payroll service fees, higher accounting fees, a California S-Corp tax, and more recordkeeping. If the all-in savings after those costs is still several thousand dollars, the S-Corp may be worth considering. If the business profit is closer to $60,000 or $80,000, the savings may disappear once compliance costs are included.

This is also where California gross receipts can change the answer. An LLC with more than $250,000 of California total income may face an additional LLC fee. That does not automatically make an S-Corp better, but it gives the owner another cost to model. A clean comparison should include federal payroll tax, California entity tax, the LLC fee if applicable, payroll software, CPA fees, and administrative time.

The Break-Even Point Is Usually About Profit, Not Revenue

Revenue alone does not answer the entity question. A company with $500,000 of revenue and $470,000 of expenses may not benefit from an S-Corp election. A lean consulting firm with $220,000 of revenue and $170,000 of profit might be a stronger candidate.

The practical question is: after paying a reasonable salary, is there enough profit left to distribute? If the answer is yes, the S-Corp analysis becomes more attractive. If the business needs every dollar of profit for owner compensation, the election may add complexity without producing much benefit.

This is why entity planning should connect to broader business tax planning, bookkeeping quality, payroll setup, and cash flow forecasting. The tax structure should support how the business actually operates.

When an LLC May Be the Better Choice

An LLC may be the better fit when the business is new, profit is inconsistent, ownership is simple, or the owner wants flexibility before committing to payroll and S-Corp compliance. Many founders start with an LLC because it is straightforward to operate and can later evaluate whether an S-Corp election makes sense.

An LLC can also be appropriate when the owner does not yet have predictable income. S-Corp payroll works best when the business can support regular salary payments. If cash flow swings widely month to month, payroll obligations can create stress.

The LLC structure may also be more flexible for partnerships, investors, special allocations, or businesses that expect ownership changes. An S-Corp has eligibility rules, shareholder restrictions, and one class of stock. Those limits may not matter for a solo consultant, but they can matter for businesses planning to add partners or raise capital.

For owners still forming or maintaining an entity, Clear Peak Accounting offers entity formation and maintenance support that can help align the legal structure with tax and compliance requirements.

When an S-Corp May Be the Better Choice

An S-Corp may be worth evaluating when the business has consistent profit, the owner works in the company, and a reasonable salary still leaves profit available for distributions. This often applies to consultants, agencies, professional services firms, medical practices, creative businesses, and other service-based companies with healthy margins.

The S-Corp structure can also create discipline. Payroll forces owner compensation into a predictable system, which can improve tax withholding and cash flow planning. But that structure only helps when the business is ready for it. If bookkeeping is behind or payroll is not properly managed, the S-Corp can create more risk than savings.

Timing matters too. An S-Corp election is not only a tax calculation. It affects payroll setup, owner draws, year-end planning, retirement contributions, health insurance treatment, and how profits are documented. The best time to evaluate the election is before the year gets too far along, when there is still time to set payroll correctly and forecast the full-year result.

Clear Peak Accounting also provides S-Corp tax advisory services for businesses that want help modeling the election, setting compensation, and managing the ongoing requirements.

Compliance Overhead: The Cost Many Owners Forget

The S-Corp tax conversation often focuses on savings, but compliance is just as important. An S-Corp owner-employee needs payroll registration, payroll tax deposits, W-2 reporting, bookkeeping that separates salary from distributions, and an annual S-Corp tax return. The business should also document how reasonable compensation was determined.

Those steps are manageable, but they are not optional. A poorly run S-Corp can create payroll tax problems, late filing penalties, and messy records. If you are comparing entities, include the cost of professional bookkeeping, payroll support, and tax preparation in the calculation.

That is where a CPA-led approach matters. Clear Peak Accounting combines business accounting and management with tax planning, so the entity decision is based on real numbers rather than a rule of thumb.

How to Decide Between an S-Corp and LLC

The right structure should match the way the business earns profit, pays owners, handles compliance, and plans for growth. Use these questions to start the conversation:

- What is your expected annual profit after ordinary expenses? Profit drives the S-Corp savings analysis more than revenue.

- What would a reasonable salary be for your role? The salary should be supportable, not chosen only to reduce tax.

- Will profit remain after salary? S-Corp savings depend on having distribution potential after payroll.

- Can your business handle payroll and bookkeeping requirements? If not, build that support before making the election.

- Are California LLC fees or S-Corp taxes changing the math? State costs can shift the break-even point.

- What are your long-term plans? Hiring, investors, multi-state activity, sale plans, and owner changes can all affect entity strategy.

Frequently Asked Questions About S-Corp vs LLC California Taxes

These answers address common questions California business owners ask when comparing an LLC and an S-Corp election.

Is an S-Corp always better than an LLC for California taxes?

No. An S-Corp is not always better than an LLC for California taxes. An S-Corp can reduce self-employment tax when the business has enough profit after a reasonable owner salary, but it also adds payroll, tax filing, recordkeeping, and California entity tax costs. If profits are low or inconsistent, an LLC may be the simpler and less expensive structure.

At what profit level should a California LLC consider S-Corp taxation?

There is no single profit level that works for every business. Many owners start the analysis once annual profit is consistently high enough to pay a reasonable salary and still leave meaningful distributions. The break-even point depends on the owner’s role, industry compensation, payroll costs, tax preparation costs, California entity costs, and cash flow needs.

Does an S-Corp avoid the California $800 minimum tax?

No. A California S-Corp generally remains subject to an $800 minimum franchise tax. It may also owe California’s 1.5% S-Corp tax on net income. The potential savings usually come from federal payroll tax planning, not from avoiding every California entity cost.

Can an LLC elect S-Corp tax treatment later?

Yes. An eligible LLC can often elect to be taxed as an S-Corp if it meets the requirements and files the proper election on time. The timing should be coordinated with payroll setup, bookkeeping, reasonable salary planning, and year-end tax projections.

What records should an S-Corp owner keep for reasonable compensation?

An S-Corp owner should keep records showing how salary was determined, including job duties, hours worked, industry compensation data, business profitability, payroll history, and distributions. This documentation supports the salary decision if the IRS questions whether compensation was reasonable.

The Bottom Line

For California businesses, an LLC usually wins on simplicity. An S-Corp can win on tax efficiency when profits are high enough, salary is reasonable, and the business has the systems to manage payroll and compliance correctly. The wrong answer is making the election because another business owner said it saved them money.

Clear Peak Accounting helps California business owners compare entity structures using actual financial data, not generic assumptions. If you are deciding between an LLC and S-Corp, or wondering whether your current structure still makes sense, schedule an appointment to review your numbers and plan the next step.